The CREATE MODEL statement for ARIMA_PLUS models

This document describes the CREATE MODEL statement for creating univariate

time series models in BigQuery by using SQL. Alternatively, you can use the

Google Cloud console user interface to

create a model by using a UI

(Preview) instead of constructing the SQL

statement yourself. You can use a univariate

time series model to forecast the

future value for a given column based on the analysis of historical values for

that column. You can also use univariate time series models to detect

anomalies in time series data.

- Use the

ML.FORECASTfunction to retrieve the forecasted values that were generated when you created the model. - Use the

ML.EXPLAIN_FORECASTfunction function to retrieve the forecasted values that were generated when you created the model, and compute the prediction intervals. - Use the

ML.DETECT_ANOMALIESfunction to perform anomaly detection.

For more information about supported SQL statements and functions for this model, see End-to-end user journey for time series forecasting models.

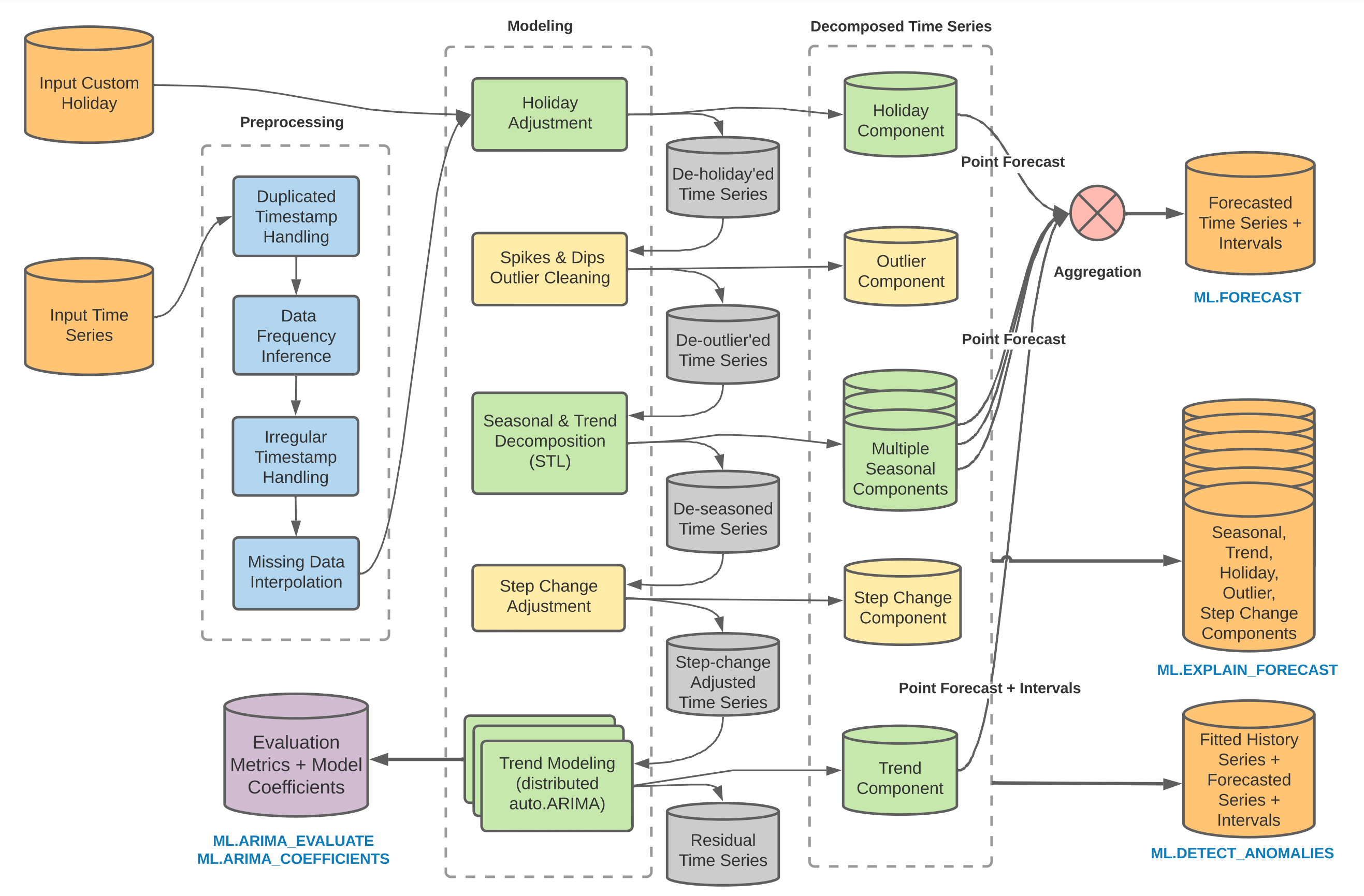

Time series modeling pipeline

The BigQuery ML time series modeling pipeline includes

multiple modules. The

ARIMA

model is the most computationally expensive module, which is why the model is

named ARIMA_PLUS.

The modeling pipeline for the ARIMA_PLUS time series models performs the

following functions:

- Infer the data frequency of the time series.

- Handle irregular time intervals.

- Handle duplicated timestamps by taking the mean value.

- Interpolate missing data using local linear interpolation.

- Detect and clean spike and dip outliers.

- Detect and adjust abrupt step (level) changes.

- Detect and adjust holiday effect.

- Detect multiple seasonal patterns within a single time series by using Seasonal and Trend decomposition using Loess (STL), and extrapolate seasonality by using double exponential smoothing (ETS).

- Detect and model the trend using the ARIMA model and the auto.ARIMA algorithm for automatic hyperparameter tuning. In auto.ARIMA, dozens of candidate models are trained and evaluated in parallel. The model with the lowest Akaike information criterion (AIC) is selected as the best model.

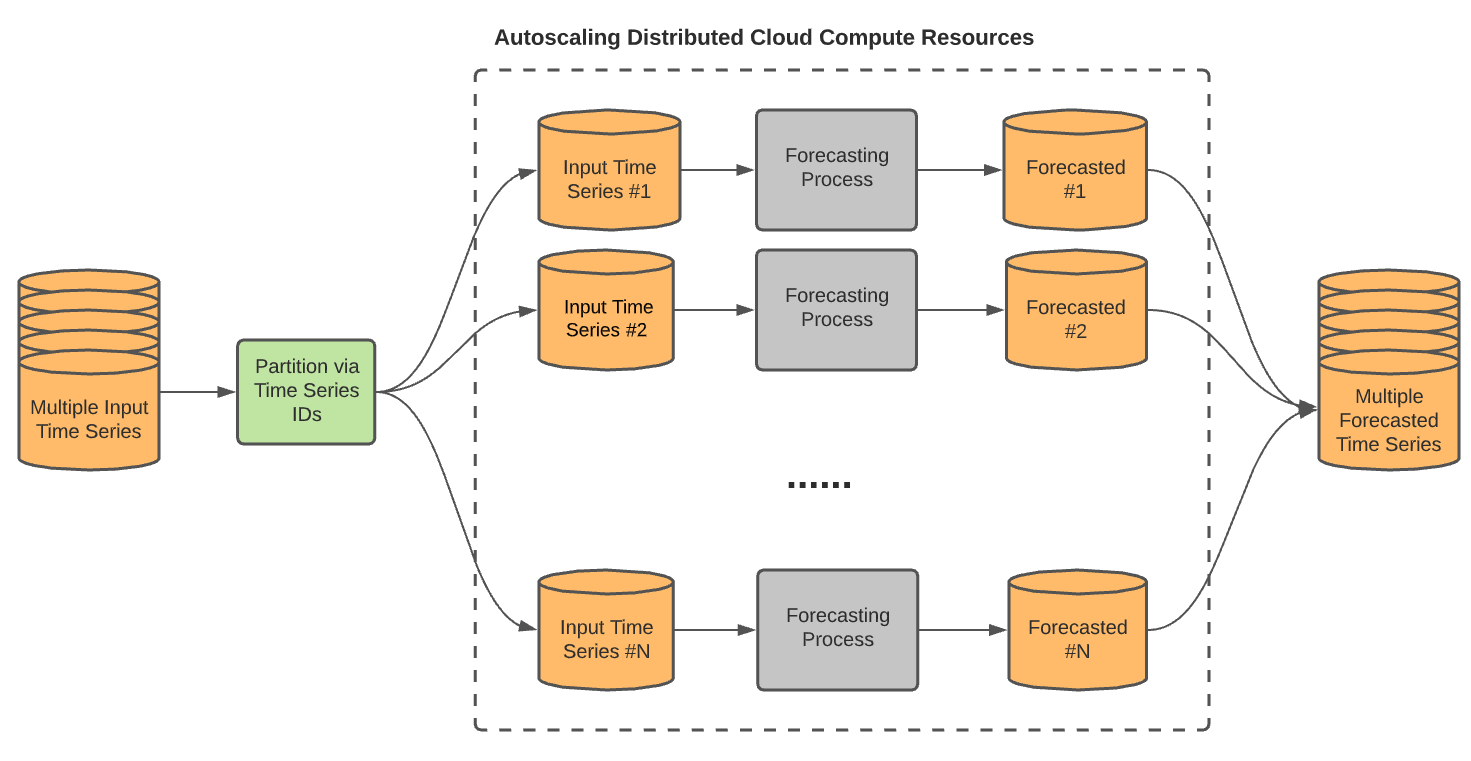

Large-scale time series

You can forecast up to 100,000,000 time series simultaneously with a single query

by using the TIME_SERIES_ID_COL

option. With this option, different modeling pipelines run in parallel, as long

as enough slots are available. The following diagram

shows this process:

Large-scale time series forecasting best practices

Forecasting many time series simultaneously can lead to long-running queries, because query processing isn't completely parallel due to limited slot capacity. The following best practices can help you avoid long-running queries when forecasting many time series simultaneously:

- When you have a large number (for example, 100,000) of time series to forecast, first forecast a small number of time series (for example, 1,000) to see how long the query takes. You can then estimate how long your entire time series forecast will take.

- You can use the

AUTO_ARIMA_MAX_ORDERoption to balance between query run time and forecast accuracy. IncreasingAUTO_ARIMA_MAX_ORDERexpands the hyperparameter search space to try more complex ARIMA models, that is, ARIMA models with higher non-seasonal p and q. This increases forecast accuracy but also increases query run time. Decreasing the value ofAUTO_ARIMA_MAX_ORDERdecreases forecast accuracy but also decreases query run time. For example, if you specify a value of3instead of using the5for this option, the query run time is reduced by at least 50%. The forecast accuracy might drop slightly for some of the time series. If a shorter training time is important to your use case, use a smaller value forAUTO_ARIMA_MAX_ORDER. - The model training time for each time series has a linear relationship to its length, which is based on the number of data points. The longer the time series, the longer the training takes. However, not all data points contribute equally to the model fitting process. Instead, the more recent the data point is, the more it contributes to the process. Therefore, if you have a long time series, for example ten years of daily data, you don't need to train a time series model using all of the data points. The most recent two or three years of data points are enough.

- You can use the

TIME_SERIES_LENGTH_FRACTION,MIN_TIME_SERIES_LENGTHandMAX_TIME_SERIES_LENGTHtraining options to enable fast model training with little to no loss of forecasting accuracy. The idea behind these options is that while periodic modeling, such as seasonality, requires a certain number of time points, trend modeling doesn't need many time points. However, trend modeling is much more computationally expensive than other time series components. By using the aforementioned training options, you can efficiently model the trend component with a subset of the time series, while the other time series components use the entire time series. - To avoid a single long-running query, use BigQuery multi-statement queries.

- In some cases, your input table might be missing values in the feature columns.

For example, in a multivariate time series with features A and B, most of the

rows contain valid values for both A and B, while some might have

NULLvalues for one or the other of the features. BigQuery ML fills in the missing values by using the mean value of the entire data column, which might include values from different time series. This causes discrepancies in the results when compared to single time series training, because the input values are affected by other time series. The best practice is to analyze the data and impute the missing feature values before runningCREATE MODEL. For example, using the mean value of that feature within each time series, or assigning a value of zero.

You can try these best practices by following the Scalable forecasting with millions of time series in BigQuery tutorial.

CREATE MODEL syntax

{CREATE MODEL | CREATE MODEL IF NOT EXISTS | CREATE OR REPLACE MODEL}

model_name

OPTIONS(model_option_list)

AS { query_statement |

(

training_data AS (query_statement),

custom_holiday AS (holiday_statement)

)

}

model_option_list:

MODEL_TYPE = 'ARIMA_PLUS'

[, TIME_SERIES_TIMESTAMP_COL = string_value ]

[, TIME_SERIES_DATA_COL = string_value ]

[, TIME_SERIES_ID_COL = { string_value | string_array } ]

[, HORIZON = int64_value ]

[, AUTO_ARIMA = { TRUE | FALSE } ]

[, AUTO_ARIMA_MAX_ORDER = int64_value ]

[, AUTO_ARIMA_MIN_ORDER = int64_value ]

[, NON_SEASONAL_ORDER = (int64_value, int64_value, int64_value) ]

[, DATA_FREQUENCY = { 'AUTO_FREQUENCY' | 'PER_MINUTE' | 'HOURLY' | 'DAILY' | 'WEEKLY' | 'MONTHLY' | 'QUARTERLY' | 'YEARLY' } ]

[, INCLUDE_DRIFT = { TRUE | FALSE } ]

[, HOLIDAY_REGION = string_value | string_array ]

[, CLEAN_SPIKES_AND_DIPS = { TRUE | FALSE } ]

[, ADJUST_STEP_CHANGES = { TRUE | FALSE } ]

[, TIME_SERIES_LENGTH_FRACTION = float64_value ]

[, MIN_TIME_SERIES_LENGTH = int64_value ]

[, MAX_TIME_SERIES_LENGTH = int64_value ]

[, TREND_SMOOTHING_WINDOW_SIZE = int64_value ]

[, DECOMPOSE_TIME_SERIES = { TRUE | FALSE } ]

[, FORECAST_LIMIT_LOWER_BOUND = float64_value ]

[, FORECAST_LIMIT_UPPER_BOUND = float64_value ]

[, SEASONALITIES = string_array ]

[, HIERARCHICAL_TIME_SERIES_COLS = {string_array } ]

[, KMS_KEY_NAME = string_value ]

CREATE MODEL

Creates and trains a new model in the specified dataset. If the model name

exists, CREATE MODEL returns an error.

CREATE MODEL IF NOT EXISTS

Creates and trains a new model only if the model doesn't exist in the specified dataset.

CREATE OR REPLACE MODEL

Creates and trains a model and replaces an existing model with the same name in the specified dataset.

model_name

The name of the model you're creating or replacing. The model name must be unique in the dataset: no other model or table can have the same name. The model name must follow the same naming rules as a BigQuery table. A model name can:

- Contain up to 1,024 characters

- Contain letters (upper or lower case), numbers, and underscores

model_name is not case-sensitive.

If you don't have a default project configured, then you must prepend the project ID to the model name in the following format, including backticks:

`[PROJECT_ID].[DATASET].[MODEL]`

For example, `myproject.mydataset.mymodel`.

MODEL_TYPE

Syntax

MODEL_TYPE = 'ARIMA_PLUS'

Description

Specifies the model type. This option is required.

TIME_SERIES_TIMESTAMP_COL

Syntax

TIME_SERIES_TIMESTAMP_COL = string_value

Description

The name of the column that provides the time points used in training the model. The column must be of one of the following data types:

TIMESTAMPDATEDATETIME

Arguments

A STRING value.

TIME_SERIES_DATA_COL

Syntax

TIME_SERIES_DATA_COL = string_value

Description

The name of the column that contains the data to forecast. The column must be of one of the following data types:

INT64NUMERICBIGNUMERICFLOAT64

Arguments

A STRING value.

TIME_SERIES_ID_COL

Syntax

TIME_SERIES_ID_COL = { string_value | string_array }

Description

The names of the ID columns. Specify one or more values for this option when you want to fit and forecast multiple time series using a single query. Each ID identifies a unique time series. The columns must be of one of the following data types:

STRINGINT64ARRAY<STRING>ARRAY<INT64>

Arguments

A STRING or ARRAY<STRING> value.

HORIZON

Syntax

HORIZON = int64_value

Description

The number of time points to forecast.

When forecasting multiple time series at once, this parameter applies to each time series.Arguments

An INT64 value. The default value is 1,000. The maximum value is 10,000.

AUTO_ARIMA

Syntax

AUTO_ARIMA = { TRUE | FALSE }

Description

Determines whether the training process uses auto.ARIMA or not. If TRUE,

training automatically finds the best non-seasonal order (that is, the p, d,

q tuple) and decides whether or not to include a linear drift term when d is 1.

If FALSE, you must specify the NON_SEASONAL_ORDER option.

TRUE.

Arguments

A BOOL value. The default value is TRUE.

AUTO_ARIMA_MAX_ORDER

Syntax

AUTO_ARIMA_MAX_ORDER = int64_value

Description

The maximum value for the sum of non-seasonal p and q. This value determines

the parameter search space in the auto.ARIMA algorithm, in combination with the

AUTO_ARIMA_MIN_ORDER value. This option is disabled when the AUTO_ARIMA

value is FALSE.

Arguments

An INT64 value between 1 and 5, inclusive. The default value is 3.

If non-seasonal d is determined to be 0 or 2, the number of candidate models evaluated for each supported value is as follows:

1: 3 candidate models2: 6 candidate models3: 10 candidate models4: 15 candidate models5: 21 candidate models

If non-seasonal d is determined to be 1, the number of candidate models to evaluate is doubled, because there's an additional drift term to consider for all of the existing candidate models.

AUTO_ARIMA_MIN_ORDER

Syntax

AUTO_ARIMA_MIN_ORDER = int64_value

Description

The minimum value for the sum of non-seasonal p and q. This value determines

the parameter search space in the auto.ARIMA algorithm, in combination with the

AUTO_ARIMA_MAX_ORDER value. Setting this option to 1 or greater lets the

model exclude some flat forecasting results. This option is disabled when

AUTO_ARIMA is FALSE.

Arguments

The value is a INT64. The default value is 0.

NON_SEASONAL_ORDER

Syntax

NON_SEASONAL_ORDER = (p_value, d_value, q_value)

Description

The tuple of non-seasonal p, d, q for the ARIMA_PLUS model. There are no

default values, and you must specify all three values. p and q must be a value

between 0 and 5, inclusive. d must be a value between 0 and 2,

inclusive.

The AUTO_ARIMA value must be FALSE to use this option.

Arguments

A tuple of three INT64 values. For example, (1, 2, 1).

DATA_FREQUENCY

Syntax

DATA_FREQUENCY = { 'AUTO_FREQUENCY' | 'PER_MINUTE' | 'HOURLY' | 'DAILY' | 'WEEKLY' | 'MONTHLY' | 'QUARTERLY' | 'YEARLY' }

Description

The data frequency of the input time series. The finest supported granularity is

PER_MINUTE.

Arguments

This option accepts the following values:

AUTO_FREQUENCY: This is the default. The training process automatically infers the data frequency, which can be any of the other supported values for this option.PER_MINUTEHOURLYDAILYWEEKLYMONTHLYQUARTERLYYEARLY

INCLUDE_DRIFT

Syntax

INCLUDE_DRIFT = { TRUE | FALSE }

Description

Determines whether the ARIMA_PLUS model should include a linear drift term or

not. The drift term is applicable when non-seasonal d is 1.

- When the

AUTO_ARIMAvalue isFALSE, this argument defaults toFALSE. You can set it toTRUEonly when non-seasonal d is 1. Otherwise theCREATE MODELstatement returns an invalid query error. - When the

AUTO_ARIMAvalue isTRUE, BigQuery ML automatically determines whether or not to include a linear drift term, so you can't use this option.

Arguments

A BOOL value. The default value is FALSE.

HOLIDAY_REGION

Syntax

HOLIDAY_REGION = string_value | string_array

Description

The geographical region based on which the holiday effect is applied in modeling. By default, holiday effect modeling isn't used. To use it, specify one or more holiday regions using this option. If you include more than one region string, the union of the holidays in all the provided regions are taken into account when modeling.

Holiday effect modeling is only applicable when the time series is daily or weekly, and longer than a year. If the input time series doesn't meet these requirements, holiday effect modeling isn't used even if you specify this option.

For more information about the holidays included in each region, see Holiday data.

Arguments

A STRING or ARRAY<STRING> value.

Use a single string value to identify one region. For example:

HOLIDAY_REGION = 'GLOBAL'

Use an array of string values to identify multiple regions. For example:

HOLIDAY_REGION = ['US', 'GB']

This option accepts the following values:

Global

GLOBAL

Continental regions

NA: North AmericaJAPAC: Japan and Asia PacificEMEA: Europe, the Middle East and AfricaLAC: Latin America and the Caribbean

Countries

AE: United Arab EmiratesAR: ArgentinaAT: AustriaAU: AustraliaBE: BelgiumBR: BrazilCA: CanadaCH: SwitzerlandCL: ChileCN: ChinaCO: ColombiaCZ: CzechiaDE: GermanyDK: DenmarkDZ: AlgeriaEC: EcuadorEE: EstoniaEG: EgyptES: SpainFI: FinlandFR: FranceGB: United KingdomGR: GreeceHK: Hong KongHU: HungaryID: IndonesiaIE: IrelandIL: IsraelIN: IndiaIR: IranIT: ItalyJP: JapanKR: South KoreaLV: LatviaMA: MoroccoMX: MexicoMY: MalaysiaNG: NigeriaNL: NetherlandsNO: NorwayNZ: New ZealandPE: PeruPH: PhilippinesPK: PakistanPL: PolandPT: PortugalRO: RomaniaRS: SerbiaRU: RussiaSA: Saudi ArabiaSE: SwedenSG: SingaporeSI: SloveniaSK: SlovakiaTH: ThailandTR: TurkeyTW: TaiwanUA: UkraineUS: United StatesVE: VenezuelaVN: VietnamZA: South Africa

CLEAN_SPIKES_AND_DIPS

Syntax

CLEAN_SPIKES_AND_DIPS = { TRUE | FALSE }

Description

Determines whether or not to perform automatic spikes and dips detection and

cleanup in the ARIMA_PLUS model training pipeline. The spikes and dips are

replaced with local linear interpolated values when they're detected.

Arguments

A BOOL value. The default value is TRUE.

ADJUST_STEP_CHANGES

Syntax

ADJUST_STEP_CHANGES = { TRUE | FALSE }

Description

Determines whether or not to perform automatic step change detection and

adjustment in the ARIMA_PLUS model training pipeline.

Arguments

A BOOL value. The default value is TRUE.

TIME_SERIES_LENGTH_FRACTION

Syntax

TIME_SERIES_LENGTH_FRACTION = float64_value

Description

The fraction of the interpolated length of the time series that's used to

model the time series trend component. All of the time points of the time series

are used to model the non-trend component. For example, if the time series has

100 time points, then specifying a TIME_SERIES_LENGTH_FRACTION of 0.5 uses

the most recent 50 time points for trend modeling. This training option

accelerates modeling training without sacrificing much forecasting accuracy.

You can use the TIME_SERIES_LENGTH_FRACTION option with the

MIN_TIME_SERIES_LENGTH option, but not with the MAX_TIME_SERIES_LENGTH

option.

Arguments

A FLOAT64 value in the range (0, 1). The default behavior is to use all

the points in the time series.

MIN_TIME_SERIES_LENGTH

Syntax

MIN_TIME_SERIES_LENGTH = int64_value

Description

The minimum number of time points that are used in modeling the

trend component of the time series. If you use this option, you must also

specify a value for the TIME_SERIES_LENGTH_FRACTION option, and you can't

specify a value for the MAX_TIME_SERIES_LENGTH option.

TIME_SERIES_ID_COL to forecast two time series, one with 100 time

points and another with 30 time points, then setting

TIME_SERIES_LENGTH_FRACTION to 0.5 and MIN_TIME_SERIES_LENGTH to 20

results in the last 50 points of first time series being used for trend

modeling. For the second time series, the last 20 points rather than the last

15 points (30 * 0.5) are used in trend modeling because

the MIN_TIME_SERIES_LENGTH value is 20. This option ensures that enough

time points are available when you use TIME_SERIES_LENGTH_FRACTION in trend

modeling. This is particularly important

when forecasting multiple time series

in a single query using the TIME_SERIES_ID_COL option. If the total number of

time points is less than the MIN_TIME_SERIES_LENGTH value, then the query uses

all available time points.

Arguments

An INT64 value greater than or equal to 4. The default value is 20.

MAX_TIME_SERIES_LENGTH

Syntax

MAX_TIME_SERIES_LENGTH = int64_value

Description

The maximum number of time points in a time series that can be used in modeling the trend component of the time series.

For example, if you are forecasting two time series simultaneously by specifying theTIME_SERIES_ID_COL option,

and one time series has 100 time points while the other one has 50 time points,

then by setting MAX_TIME_SERIES_LENGTH to 30, both of the time series use

the last 30 time points for trend modeling.

You can't use theMAX_TIME_SERIES_LENGTH with the

TIME_SERIES_LENGTH_FRACTION or MIN_TIME_SERIES_LENGTH options.

Arguments

An INT64 value greater than or equal to 4. There is no default

value. We recommend trying 30 as a starting value.

TREND_SMOOTHING_WINDOW_SIZE

Syntax

TREND_SMOOTHING_WINDOW_SIZE = int64_value

Description

The smoothing window size for the trend component. When you specify a value, a center moving average smoothing is applied on the history trend. When the smoothing window is out of the boundary at the beginning or the end of the trend, the first element or the last element is padded to fill the smoothing window before the average is applied.

Specifying a value for TREND_SMOOTHING_WINDOW_SIZE doesn't affect forecasting

results. It only affects the smoothness of the trend component, which you can

see by using the

ML.EXPLAIN_FORECAST function.

Arguments

An INT64 value. There is no default value. You must specify a positive value

to smooth the trend.

DECOMPOSE_TIME_SERIES

Syntax

DECOMPOSE_TIME_SERIES = { TRUE | FALSE }

Description

Determines whether the separate components of both the history and forecast

parts of the time series (such as holiday effect and seasonal components)

are saved in the ARIMA_PLUS model.

Time series decomposition takes place when you create the model. The

ML.EXPLAIN_FORECAST

function retrieves the separate components of both the training and the

forecasting data and computes the confidence intervals. Because the decomposition

results are saved in the model, the training data can be partially or fully

recovered from the decomposition results.

Arguments

A BOOL value. The default value is TRUE.

FORECAST_LIMIT_LOWER_BOUND

Syntax

FORECAST_LIMIT_LOWER_BOUND = float64_value

Description

The lower bound of the forecasting values. When you specify the

FORECAST_LIMIT_LOWER_BOUND option, all of the forecast values must be greater

than the specified value. For example, if you set FORECAST_LIMIT_LOWER_BOUND

to 0, then all of the forecast values are larger than 0. Also, all values

less than or equal to the FORECAST_LIMIT_LOWER_BOUND value are excluded from

modelling. The forecasting limit

ensures that forecasts stay within limits.

If you specify a value for theFORECAST_LIMIT_UPPER_BOUND option,

the FORECAST_LIMIT_UPPER_BOUND value must be greater than the

FORECAST_LIMIT_LOWER_BOUND value.

Arguments

A FLOAT_64 value greater than or equal to -1.7976931348623157E+308.

FORECAST_LIMIT_UPPER_BOUND

Syntax

FORECAST_LIMIT_UPPER_BOUND = float64_value

Description

The upper bound of the forecasting values. When you specify the

FORECAST_LIMIT_UPPER_BOUND option, all of the forecast values must be less

than the specified value. For example, if you set FORECAST_LIMIT_UPPER_BOUND

to 100, then all of the forecast values are less than 100. Also, all values

greater than or equal to the FORECAST_LIMIT_UPPER_BOUND value are excluded

from modelling. The forecasting limit ensures that

forecasts stay within limits.

If you specify a value for theFORECAST_LIMIT_LOWER_BOUND option,

the FORECAST_LIMIT_LOWER_BOUND value must be less than the

FORECAST_LIMIT_UPPER_BOUND value.

Arguments

A FLOAT_64 value less thanor equal to 1.7976931348623157E+308.

SEASONALITIES

Syntax

SEASONALITIES = string_array

Description

The seasonality of the time series data refers to the presence of variations

that occur at certain regular intervals such as weekly, monthly or quarterly.

Specifying the seasonality helps the model more accurately learn and predict the

cyclic trends in your data. The input seasonality you provide as an argument is

ignored if it's more granular than the finest seasonal granularity detected in

the time series data. For example, if you input ['DAILY', 'WEEKLY', 'MONTHLY']

for this option, but input time series contains weekly data, then

the DAILY variable is ignored during the model training.

Arguments

An ARRAY<STRING> value. The following string values are accepted:

AUTO: This is the default. The training process automatically infers the seasonalities by data frequency.NO_SEASONALITY: Deactivates automatic seasonality detection.DAILYWEEKLYMONTHLYQUARTERLYYEARLY

You can only use the NO_SEASONALITY or AUTO values by themselves. For

example, ['NO_SEASONALITY', 'DAILY'] isn't a valid value for this option.

HIERARCHICAL_TIME_SERIES_COLS

Syntax

HIERARCHICAL_TIME_SERIES_COLS = { string_array }

Description

The column names used to generate hierarchical time series forecasts. Specify one or more values for this option to aggregate and roll up values for all time series. The column order represents the hierarchy structure, where the left-most column is the parent. The columns must be of one of the following data types:

STRINGINT64

Arguments

An ARRAY<STRING> value.

KMS_KEY_NAME

Syntax

KMS_KEY_NAME = string_value

Description

The Cloud Key Management Service customer-managed encryption key (CMEK) to use to encrypt the model.

Arguments

A STRING value containing the fully-qualified name of the CMEK. For example,

'projects/my_project/locations/my_location/keyRings/my_ring/cryptoKeys/my_key'

AS

All time series forecasting models support the following AS clause

syntax for specifying the training data:

AS query_statement

For time series forecasting models that have a DATA_FREQUENCY value

of either DAILY or AUTO_FREQUENCY, you can optionally use the

following AS clause syntax to perform

custom holiday modeling

in addition to specifying the training data:

AS ( training_data AS (query_statement), custom_holiday AS (holiday_statement) )

query_statement

The query_statement argument specifies the query that is used to

generate the training data. For information about the supported SQL syntax of

the query_statement clause, see

GoogleSQL query syntax.

holiday_statement

The holiday_statement argument specifies the query that provides custom

holiday modeling information for time series forecast models. This query must

return 50,000 rows or less and must contain the following columns:

region: Required. ASTRINGvalue that identifies the region to target for holiday modeling. Use one of the following options:- An upper-case

holiday region code.

Use this option to

overwrite or supplement the holidays for the specified region. You

can see the holidays for a region by running

SELECT * FROM bigquery-public-data.ml_datasets.holidays_and_events_for_forecasting WHERE region = region. - An arbitrary string. Use this option to specify a custom region that

you want to model holidays for. For example, you could specify

Londonif you are only modeling holidays for that city.

Be sure not to use an existing holiday region code when you are trying to model for a custom region. For example, if you want to model a holiday in California, and specify

CAas theregionvalue, the service recognizes that as the holiday region code for Canada and targets that region. Because the argument is case-sensitive, you could specifyca,California, or some other value that isn't a holiday region code.- An upper-case

holiday region code.

Use this option to

overwrite or supplement the holidays for the specified region. You

can see the holidays for a region by running

holiday_name: Required. ASTRINGvalue that identifies the holiday to target for holiday modeling. Use one of the following options:- The holiday name as it is represented in the

bigquery-public-data.ml_datasets.holidays_and_events_for_forecastingpublic table, including case. Use this option to overwrite or supplement the specified holiday. - A string that represents a custom holiday. The string must be a valid

column name so that it can be used in

ML.EXPLAIN_FORECASToutput. For example, it cannot contain space. For more information on column naming, see Column names.

- The holiday name as it is represented in the

primary_date: Required. ADATEvalue that specifies the date the holiday falls on.preholiday_days: Optional. AnINT64value that specifies the start of the holiday window around the holiday that is taken into account when modeling. Must be greater than or equal to1. Defaults to1.postholiday_days: Optional. AnINT64value that specifies the end of the holiday window around the holiday that is taken into account when modeling. Must be greater than or equal to1. Defaults to1.

The preholiday_days and postholiday_days arguments together describe

the holiday window around the holiday that is taken into account

when modeling. The holiday window is defined as

[primary_date - preholiday_days, primary_date + postholiday_days] and is

inclusive of the pre- and post-holiday days. The value for each holiday window

must be less than or equal to 30 and must be the same across the given

holiday. For example, if you are modeling Arbor Day for several different years,

you must specify the same holiday window for all of those years.

To achieve the best holiday modeling result, provide as much historical and forecast information about the occurrences of each included holiday as possible. For example, if you have time series data from 2018 to 2022 and would like to forecast for 2023, you get the best result by providing the custom holiday information for all of those years, similar to the following:

CREATE OR REPLACE MODEL `mydataset.arima_model` OPTIONS ( model_type = 'ARIMA_PLUS', holiday_region = 'US',...) AS ( training_data AS (SELECT * FROM `mydataset.timeseries_data`), custom_holiday AS ( SELECT 'US' AS region, 'Halloween' AS holiday_name, primary_date, 5 AS preholiday_days, 1 AS postholiday_days FROM UNNEST( [ DATE('2018-10-31'), DATE('2019-10-31'), DATE('2020-10-31'), DATE('2021-10-31'), DATE('2022-10-31'), DATE('2023-10-31')]) AS primary_date ) )

Holiday data

When you perform holiday modeling by specifying the HOLIDAY_REGION option,

the model uses holiday data from the region or regions you specify. For example,

the following table describes the holiday data used in the US region for the

year 2022-2023.

regionspecifies the geographic region to which the holiday applies. The supported regions are listed inHOLIDAY_REGION.holiday_namecontains the name of the holiday.primary_datespecifies the date of the holiday. For holidays that span multiple days, this is usually the first day of the holiday.preholiday_daysdescribes the number of days the holiday effect starts before theprimary_datevalue.postholiday_daysdescribes the number of days the holiday effect ends after theprimary_datevalue.

| region | holiday_name | primary_date | preholiday_days | postholiday_days |

|---|---|---|---|---|

| US | Christmas | 2022-12-25 | 10 | 1 |

| US | Christmas | 2023-12-25 | 10 | 1 |

| US | MothersDay | 2022-05-08 | 6 | 1 |

| US | MothersDay | 2023-05-14 | 6 | 1 |

| US | NewYear | 2022-01-01 | 5 | 3 |

| US | NewYear | 2023-01-01 | 5 | 3 |

| US | DaylightSavingEnd | 2022-11-06 | 1 | 1 |

| US | DaylightSavingEnd | 2023-11-05 | 1 | 1 |

| US | DaylightSavingStart | 2022-03-13 | 1 | 1 |

| US | DaylightSavingStart | 2023-03-12 | 1 | 1 |

| US | Thanksgiving | 2022-11-24 | 3 | 5 |

| US | Thanksgiving | 2023-11-23 | 3 | 5 |

| US | Valentine | 2022-02-14 | 3 | 1 |

| US | Valentine | 2023-02-14 | 3 | 1 |

| US | EasterMonday | 2022-04-18 | 8 | 1 |

| US | EasterMonday | 2023-04-10 | 8 | 1 |

| US | Halloween | 2022-10-31 | 1 | 1 |

| US | Halloween | 2023-10-31 | 1 | 1 |

| US | StPatrickDay | 2022-03-17 | 1 | 1 |

| US | StPatrickDay | 2023-03-17 | 1 | 1 |

| US | ColumbusDay | 2022-10-10 | 1 | 1 |

| US | ColumbusDay | 2023-10-09 | 1 | 1 |

| US | IndependenceDay | 2022-07-04 | 1 | 1 |

| US | IndependenceDay | 2023-07-04 | 1 | 1 |

| US | Juneteenth | 2022-06-19 | 1 | 1 |

| US | Juneteenth | 2023-06-19 | 1 | 1 |

| US | LaborDay | 2022-09-05 | 1 | 1 |

| US | LaborDay | 2023-09-04 | 1 | 1 |

| US | MemorialDay | 2022-05-30 | 1 | 1 |

| US | MemorialDay | 2023-05-29 | 1 | 1 |

| US | MLKDay | 2022-01-17 | 1 | 1 |

| US | MLKDay | 2023-01-16 | 1 | 1 |

| US | PresidentDay | 2022-02-21 | 1 | 1 |

| US | PresidentDay | 2023-02-20 | 1 | 1 |

| US | Superbowl | 2022-02-13 | 1 | 1 |

| US | Superbowl | 2023-02-05 | 1 | 1 |

| US | VeteranDay | 2022-11-11 | 1 | 1 |

| US | VeteranDay | 2023-11-11 | 1 | 1 |

You can also see the holidays for a region by running SELECT * FROM

bigquery-public-data.ml_datasets.holidays_and_events_for_forecasting WHERE

region = region.

The bigquery-public-data.ml_datasets.holidays_and_events_for_forecasting

table only contains holidays and events from the following regions:

AU: AustraliaCA: CanadaCH: SwitzerlandCL: ChileCZ: CzechiaDE: GermanyDK: DenmarkEMEA: Europe, the Middle East and AfricaES: SpainFR: FranceGB: United KingdomGLOBALID: IndonesiaIN: IndiaIT: ItalyJAPAC: Japan and Asia PacificJP: JapanKR: South KoreaLAC: Latin America and the CaribbeanMX: MexicoMY: MalaysiaNA: North AmericaNL: NetherlandsNZ: New ZealandPT: PortugalSK: SlovakiaUS: United StatesZA: South Africa

Custom holidays

You can combine use of the holiday_statement argument

and the HOLIDAY_REGION option to enable several different

custom holiday scenarios, as described in the following sections.

Supplement built-in holidays with additional custom holidays

To model one or more custom holidays in addition to a region's built-in

holidays, specify the target holiday region with the HOLIDAY_REGION option,

and then provide the new holiday metadata in the holiday_statement argument.

The following example models all built-in holidays for the US holiday region,

and additionally models the custom holiday members_day:

CREATE OR REPLACE MODEL `mydataset.arima_model` OPTIONS ( model_type = 'ARIMA_PLUS', holiday_region = 'US',...) AS ( training_data AS (SELECT * FROM `mydataset`.timeseries_data`), custom_holiday AS ( SELECT 'US' AS region, 'members_day' AS holiday_name, primary_date, 2 AS preholiday_days, 2 AS postholiday_days FROM UNNEST( [ DATE('2016-06-15'), DATE('2017-06-07'), DATE('2018-06-06')]) AS primary_date ) );

Model only custom holidays

To model only custom holidays, don't specify a value for the HOLIDAY_REGION

option, and provide the new holiday metadata in the holiday_statement

argument.

The following example models only the custom holiday members_day

for the US holiday region:

CREATE OR REPLACE MODEL `mydataset.arima_model` OPTIONS ( model_type = 'ARIMA_PLUS', -- Don't specify HOLIDAY_REGION ...) AS ( training_data AS (SELECT * FROM `mydataset.timeseries_data`), custom_holiday AS ( SELECT 'US' AS region, 'members_day' AS holiday_name, primary_date, 2 AS preholiday_days, 2 AS postholiday_days FROM UNNEST( [ DATE('2016-06-15'), DATE('2017-06-07'), DATE('2018-06-06')]) AS primary_date ) );

Change the metadata for built-in holidays

You can change the primary date and holiday effect window used by the model

for one or more built-in holidays. To do this, specify the target holiday

region with the HOLIDAY_REGION option, and then provide the modified holiday

metadata in the holiday_statement argument.

The following example models all built-in holidays for the US holiday region,

but models 3 years of the EasterMonday holiday with a 3-day

holiday effect window instead of the default 9-day holiday effect window:

OPTIONS ( model_type = 'ARIMA_PLUS', holiday_region = 'US',...) AS ( training_data AS (SELECT * FROM `mydataset.timeseries_data`), custom_holiday AS ( SELECT 'US' AS region, 'EasterMonday' AS holiday_name, primary_date, 1 AS preholiday_days, 1 AS postholiday_days FROM UNNEST( [ DATE('2016-03-28'), DATE('2017-04-17'), DATE('2018-04-02')]) AS primary_date ) );

Model a subset of built-in holidays

To model only a subset of built-in holidays, don't specify a value for the

HOLIDAY_REGION option, and provide a query based on the

bigquery-public-data.ml_datasets.holidays_and_events_for_forecasting public

table to specify the set of holidays to model.

The following example models all built-in holidays for the US holiday region

except for the Christmas and NewYears holidays:

CREATE OR REPLACE MODEL `mydataset.arima_model` OPTIONS ( model_type = 'ARIMA_PLUS', -- Don't specify HOLIDAY_REGION ...) AS ( training_data AS (SELECT * FROM `mydataset.timeseries_data`), custom_holiday AS ( SELECT * FROM `bigquery-public-data.ml_datasets.holiday` WHERE region = 'US' AND (holiday_name != 'Christmas' OR holiday_name != 'NewYear') ) );

Custom holiday limitations

- Custom holiday modeling only works for models that have a

data_frequencyvalue of eitherDAILYorAUTO_FREQUENCY. If you useAUTO_FREQUENCY, the actual frequency of the time series data needs to be daily. - You can't use the

TRANSFORMclause of theCREATE MODELstatement if you are performing custom holiday modeling. holiday_namecolumn cannot have more than 500 distinct values.- Custom holiday modeling uses an algorithm that automatically

detects the significance of the holiday effect within the provided holiday

effect window, and only extracts the holiday effect on the days that the

algorithm classifies as significant. For example, if

primary dateis01/02withpreholiday_daysandpostholiday_daysset to1, the algorithm analyzes the holiday effect for these three days:[01/01, 01/02, 01/03]. In theML.EXPLAIN_FORECASToutput, it is not guaranteed that all three of these days will have a holiday effect. Only those days within this window that have a significant holiday effect are associated with a non-zero holiday effect in the output. - To get a better result from custom holiday modeling, don't specify the same holiday more than twice a year.

- If you specify the same holiday more than once, make sure its occurrences don't overlap. For example, a holiday that happens twice a year, with the first occurrence from December 1 - December 5 and the second occurrence from December 4 - December 8, won't work because these two occurrences overlap with each other on December 4 and December 5.

- Different holidays can have partial overlap with each other, but full overlap isn't allowed. For example, if holiday A has an occurrence from December 1 - December 5, then holiday B can have an occurrence from December 4 - December 8. However, holiday B can't have an occurrence from December 2 - December 4, which is fully within holiday A's occurrence, and holiday B can't have an occurrence from December 1 - December 8, which overlaps with all of holiday A's occurrence.

- In cases where holidays overlap for a period, the overlap between the holidays can't be identical in multiple years. If it is, then it isn't possible to determine each holiday's effect on the overlapped period. For example, suppose holiday A and holiday B overlap from December 2 - December 4 in 2024, and the time series has three years of data from 2022-2024. Holidays A and B can't overlap from December 2 - December 4 in 2023 and 2022 as well if you want to be able to determine the holiday effect for each.

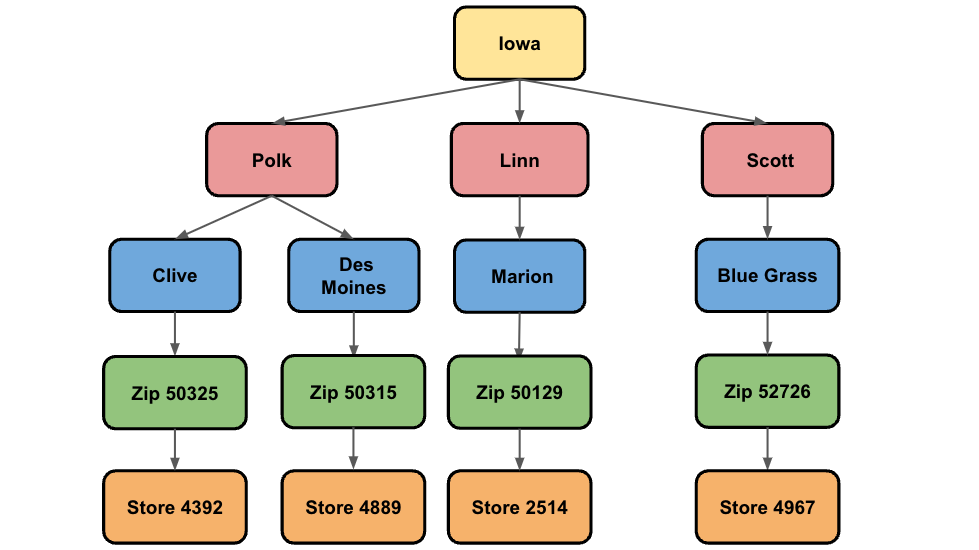

Hierarchical reconciliation

You can break down or aggregate time series forecasts by specifying different dimensions of interest. These are known as hierarchical time series. For example, census data that reveals the total population per state can be broken down by city and zip code. Conversely, you can aggregate that data for each country or continent.

There are several techniques that you can use to generate and reconcile hierarchical forecasts. Take the following example, which shows a simplified hierarchical structure for liquor sales in the state of Iowa:

The lowest level shows the store level, followed by the zip code level, city, county, and finally by state. The goal for hierarchical forecasts is to make sure that all forecasts across each level reconcile. For example, given the earlier figure, this means that the forecast values for the cities of Clive and Des Moines must add up to the forecast value for Polk county. Similarly, the forecasts in Polk, Linn, and Scott must add up to the forecast in Iowa.

A common technique that you can use to generate reconciled forecasts is known

as the Bottom-Up approach. In this approach, the forecasts are generated at

the bottom level of the hierarchy first, before summing up the other levels.

Taking the earlier example, the forecasts for each store are used to build the

forecasting models for the other levels, so the store models are used to build

the zip code models, the zip code models are used to build the city models,

and so forth.

In BigQuery ML, you use the

TIME_SERIES_ID_COL option to identify the dimensions

that you want to generate time series for, and the

HIERACHICAL_TIME_SERIES_ID_COLS option

to identify the dimensions that you want to roll up and reconcile. To learn

more about generating a hierarchical time series, see

Forecast multiple hierarchical time series with a univariate model.

Locations

For information about supported locations, see Locations for non-remote models.

Limitations

ARIMA_PLUS models have the following limitations:

- For the input time series, the minimum length is 3 time points. The maximum

length is 500,000 time points when the

DECOMPOSE_TIME_SERIESoption is setTRUEand 1,000,000 when the option is set toFALSE. When forecasting multiple time series at the same time, the limit applies to each time series. - The maximum number of time series to forecast simultaneously using the ID columns is 100,000,000.

- When forecasting multiple time series simultaneously using the ID column,

any invalid time series that fail the model fitting are ignored and

don't appear in the results of forecast. For example, a single point

time series. A warning message is shown in this case, and you can use the

ML.ARIMA_EVALUATEfunction to retrieve the error message. - The maximum time points to forecast is 10,000.

- Holiday effect modeling is effective only for approximately 5 years.

- After a multiple time series model is trained, the evaluation tab in the

BigQuery page on the Google Cloud console only shows the evaluation

metrics for the first 100 time series. To see the evaluation metrics for all

of the time series, use the

ML.ARIMA_EVALUATEfunction. - You can't export

ARIMA_PLUSmodels.

Examples

The following examples show how to create different types of ARIMA_PLUS

time series models.

Forecast a single time series

This example shows how to create a time series model that forecasts a single time series:

CREATE MODEL `project_id.mydataset.mymodel` OPTIONS(MODEL_TYPE='ARIMA_PLUS', time_series_timestamp_col='date', time_series_data_col='transaction') AS SELECT date, transaction FROM `mydataset.mytable`

Forecast multiple time series

This example shows how to create multiple time series models, one for each input time series:

CREATE MODEL `project_id.mydataset.mymodel` OPTIONS(MODEL_TYPE='ARIMA_PLUS', time_series_timestamp_col='date', time_series_data_col='transaction', time_series_id_col='company_name') AS SELECT date, transaction, company_name FROM `mydataset.mytable`

Forecast multiple time series using multiple time series ID columns

This example shows how to create multiple time series models for multiple IDs:

CREATE MODEL `project_id.mydataset.mymodel` OPTIONS(MODEL_TYPE='ARIMA_PLUS', time_series_timestamp_col='date', time_series_data_col='transaction', time_series_id_col=['company_name', 'department_name']) AS SELECT date, transaction, company_name, department_name FROM `mydataset.mytable`

Forecast multiple time series more quickly by using a fraction of the time points

This example shows how to create multiple time series models while

improving training speed by using the TIME_SERIES_LENGTH_FRACTION and

MIN_TIME_SERIES_LENGTH options:

CREATE MODEL `project_id.mydataset.mymodel` OPTIONS(MODEL_TYPE='ARIMA_PLUS', time_series_timestamp_col='date', time_series_data_col='transaction', time_series_id_col=['company_name', 'department_name'], time_series_length_fraction=0.5, min_time_series_length=30) AS SELECT date, transaction, company_name, department_name FROM `mydataset.mytable`

Forecast multiple time series more quickly by defining a maximum number of time points

This example shows how to create multiple time series models while

improving training speed by using MAX_TIME_SERIES_LENGTH option:

CREATE MODEL `project_id.mydataset.mymodel` OPTIONS(MODEL_TYPE='ARIMA_PLUS', time_series_timestamp_col='date', time_series_data_col='transaction', time_series_id_col=['company_name', 'department_name'], max_time_series_length=50) AS SELECT date, transaction, company_name, department_name FROM `mydataset.mytable`

What's next

- Try the following tutorials to learn more about creating time series models:

- Perform single time series forecasting from Google Analytics data

- Perform multiple time series forecasting with a single query from NYC Citi Bike trips data

- Scalable forecasting with millions of time series in BigQuery

- Use custom holidays in a time series forecasting model

- Limit forecasted values for a time series model

- Hierarchical time series forecasting

- Explore a notebook solution that helps you build a time series demand forecasting model.